Retirement planning is crucial for financial security in later years. Two of the most common retirement accounts are Individual Retirement Accounts (IRAs) and 401(k)s. Understanding their differences can help individuals make informed choices about their financial futures. This blog post will explore the essential aspects of both accounts, their benefits, and how to utilize them effectively for retirement savings.

Introduction to Retirement Accounts

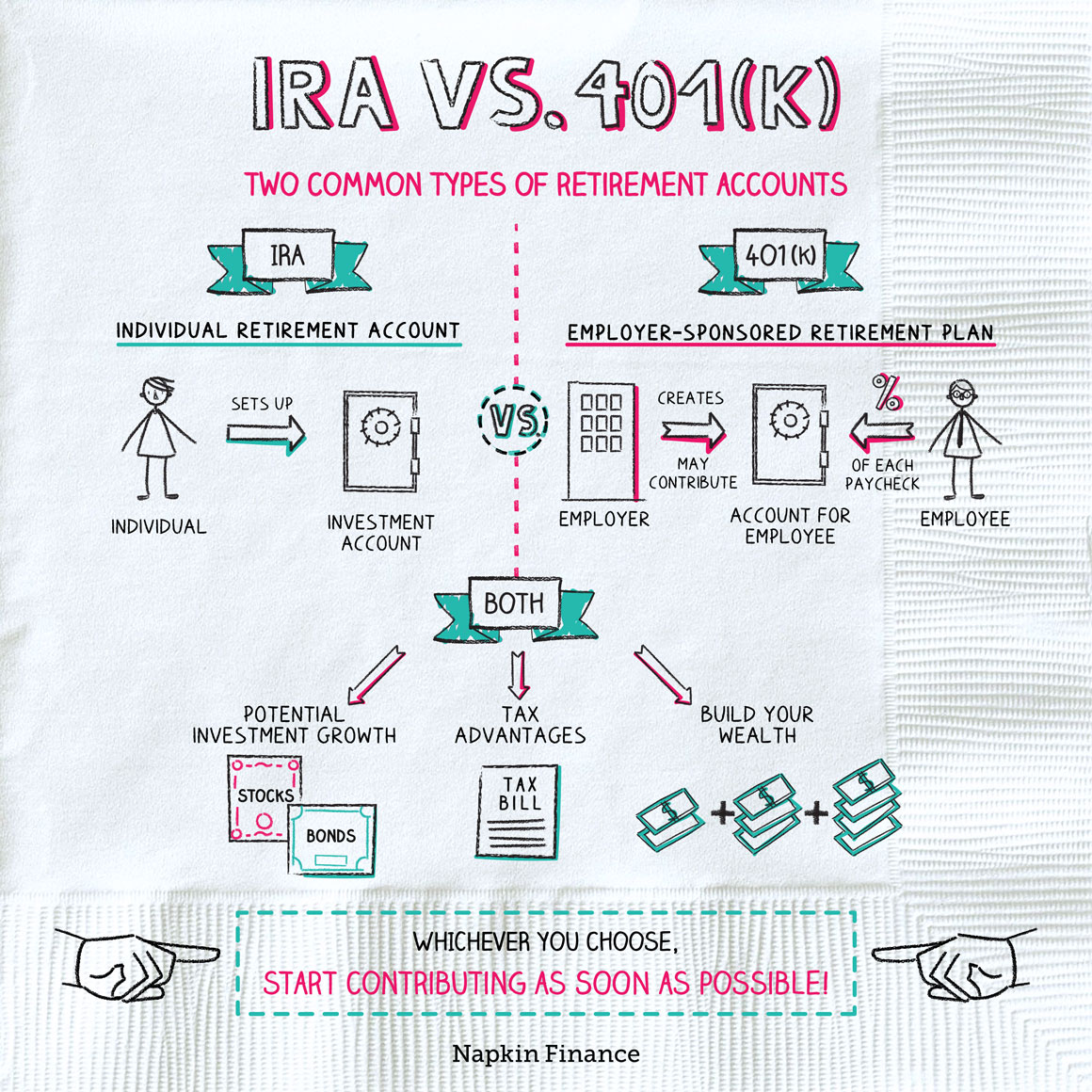

Retirement accounts are designed to help individuals save money for their retirement years, providing tax advantages and investment opportunities. Individual Retirement Accounts (IRAs) and 401(k) plans serve as two primary vehicles for retirement savings in the United States. An IRA is an account that individuals can set up and manage independently, while a 401(k) is typically sponsored by an employer, allowing employees to contribute a portion of their salary directly to the plan. The importance of these accounts cannot be overstated. With increasing life expectancy and the uncertainty surrounding Social Security benefits, relying solely on government programs for retirement may not be sufficient. By understanding and utilizing IRAs and 401(k)s, individuals can take proactive steps to ensure they have the financial resources needed for a comfortable retirement. Both account types offer distinct advantages, but knowing how to navigate their features is essential. This post will delve into their key differences, contribution strategies, tax implications, flexibility, investment choices, long-term planning, and common misconceptions, providing readers with a comprehensive overview of these vital retirement tools.

Key Differences Between IRA and 401(k)

A fundamental distinction between IRAs and 401(k)s is their sponsorship. A 401(k) is employer-sponsored, meaning contributions are deducted from an employee’s paycheck before taxes are taken out, while an IRA is individually managed and can be set up by anyone with earned income. Contribution limits differ significantly between the two accounts. For 2023, the contribution limit for 401(k) plans is $22,500, with an additional $7,500 catch-up contribution for those aged 50 and older. In contrast, the limit for traditional and Roth IRAs is $6,500, with a $1,000 catch-up contribution for those over 50. These limits can affect the overall amount individuals can save for retirement and should be factored into financial planning. Tax implications also vary. Contributions to a 401(k) are typically pre-tax, reducing taxable income for the year, while contributions to a traditional IRA may be tax-deductible depending on income and participation in an employer plan. Roth IRAs, however, involve post-tax contributions, allowing for tax-free withdrawals in retirement. Understanding these tax implications is crucial for optimizing retirement savings and minimizing future tax liabilities.

Contribution Strategies

Maximizing contributions to retirement accounts is essential for building wealth and ensuring a comfortable retirement. Each account type has its own contribution limits, and individuals should aim to contribute as much as possible within these limits. For those with access to a 401(k), it’s advisable to contribute enough to receive any employer matching contributions, as this is essentially “free money.” When considering how to allocate funds between IRAs and 401(k)s, individuals should evaluate their financial situation, including income, expenses, and retirement goals. A common strategy is to contribute enough to a 401(k) to take full advantage of employer matching, then direct additional savings into an IRA. This approach allows individuals to benefit from both tax advantages and investment options available in each account. Additionally, individuals should regularly review their contributions and adjust them as necessary. Life events such as salary increases or changes in financial goals can provide opportunities to increase retirement savings. Utilizing automatic contributions and setting annual reminders to reassess contribution levels can further enhance retirement savings efforts.

Tax Implications of Each Account

Both IRAs and 401(k)s offer significant tax advantages, but they operate differently. Contributions to a 401(k) are typically made with pre-tax dollars, meaning they reduce an individual’s taxable income in the year they are made. This can be particularly beneficial for those in higher tax brackets, as it lowers their immediate tax burden. In contrast, traditional IRAs may offer tax-deductible contributions depending on the individual’s income level and participation in an employer-sponsored retirement plan. Roth IRAs, on the other hand, do not provide an upfront tax deduction; contributions are made with after-tax dollars, but qualified withdrawals in retirement are tax-free. This can be advantageous for individuals who anticipate being in a higher tax bracket during retirement. Understanding the tax implications of retirement accounts is vital for effective financial planning. Individuals should consider their current and anticipated future tax situations when deciding between traditional and Roth accounts. It may also be beneficial to consult with a tax professional to navigate these complexities and maximize tax benefits.

Flexibility and Access to Funds

Accessing retirement funds can vary significantly between IRAs and 401(k)s. Generally, IRAs offer greater flexibility when it comes to withdrawals. Traditional IRAs typically allow penalty-free withdrawals for certain circumstances, such as first-time home purchases or qualified education expenses. However, early withdrawals (before age 59½) usually incur a 10% penalty, along with applicable taxes. 401(k) plans, while offering some flexibility, often have stricter rules regarding withdrawals. Many plans require individuals to reach age 59½ before accessing funds without penalties. Additionally, some plans may allow loans or hardship withdrawals, but these options can come with limitations and potential tax implications. Understanding the rules governing withdrawals from both accounts is essential for effective retirement planning. Individuals should consider their potential need for liquidity and access to funds when choosing between an IRA and a 401(k). Planning for emergencies and life events can help mitigate the impact of penalties and taxes associated with early withdrawals.

Investment Choices and Control

Control over investment choices is a crucial factor for many investors when selecting between IRAs and 401(k)s. 401(k) plans typically limit investment options to a selection of funds chosen by the employer or plan administrator. This can restrict individual investors’ ability to tailor their portfolios according to their risk tolerance and investment preferences. Conversely, IRAs offer a broader range of investment choices, allowing individuals to invest in stocks, bonds, mutual funds, exchange-traded funds (ETFs), real estate, and even alternative investments such as cryptocurrencies. This flexibility can empower investors to create a diversified portfolio that aligns with their financial goals and risk appetite. However, with greater investment freedom comes increased responsibility. Individuals managing IRAs must take the time to research and select appropriate investments, monitor performance, and adjust their strategies as needed. Understanding one’s investment preferences and willingness to actively manage a portfolio is essential when choosing between an IRA and a 401(k).

Long-Term Planning and Retirement Goals

Effective retirement planning requires a clear understanding of personal financial goals. Individuals should evaluate their long-term objectives, including desired lifestyle, income needs, and risk tolerance. This self-assessment helps in determining how much to save and which retirement accounts to prioritize. It’s also essential to recognize that retirement goals may evolve over time due to changes in personal circumstances, such as marriage, children, career advancements, or health issues. Regularly revisiting and adjusting retirement strategies is crucial to staying on track. Individuals should consider working with financial advisors to create a comprehensive retirement plan that incorporates both IRAs and 401(k)s. Professional guidance can provide valuable insights into asset allocation, tax strategies, and investment choices that align with retirement goals.

Common Misconceptions and Mistakes

Many individuals hold misconceptions about retirement accounts that can hinder their financial planning. One common myth is that one account type is universally better than the other. In reality, the best choice depends on individual circumstances, including income level, employer benefits, and personal financial goals. Another mistake is underestimating the impact of employer matching contributions in 401(k) plans. Failing to contribute enough to receive the full match can result in significant lost savings over time. Additionally, some individuals may not take full advantage of the tax benefits associated with IRAs, either by contributing too little or selecting the wrong type of account. Educating oneself about these accounts and avoiding common pitfalls is essential for effective retirement planning. By understanding the nuances of IRAs and 401(k)s, individuals can make informed decisions that will positively impact their financial futures.

Conclusion and Next Steps

In conclusion, understanding the nuances between IRAs and 401(k)s is vital for effective retirement planning. Each account type offers distinct advantages and drawbacks, and individuals should carefully consider their financial situations and long-term goals when making decisions. To optimize retirement savings, individuals should assess their current contributions, explore employer matching opportunities, and stay informed about tax implications. Regularly reviewing retirement strategies and making adjustments as life circumstances change can help ensure a secure financial future. Lastly, consulting with financial professionals can provide valuable insights and personalized advice tailored to individual needs. By taking proactive steps today, individuals can lay the groundwork for a comfortable and fulfilling retirement. For more detailed information, consider exploring resources such as Retirement Plans on Wikipedia.